Calgary Alberta - STB has already decided that CP's proposed use of a voting trust is subject to the pre-2001 merger rules, which entails different standards and processes than those governing CN proposal for review under current regulations. Today, Canadian Pacific Railway Limited (CP) filed the following letter with the Surface Transportation Board:

The Honorable Cynthia T. Brown

Chief, Section of Administration, Office of Proceedings

Surface Transportation Board

395 E Street S.W.

Washington, DC 20423

Re: Finance Docket No. 36500, Canadian Pacific Ry. - Control - Kansas City Southern

Finance Docket No. 36514, Canadian National Ry. - Control - Kansas City Southern

Dear Ms. Brown:

I am writing on behalf of the Canadian Pacific Applicants in Finance Docket No. 36500,[1] in response to the letter submitted by Canadian National (CN) on 26 Apr 2021 in the above-referenced dockets. In that submission, CN asks the Board to subject the voting trust arrangement proposed by CP for its acquisition of Kansas City Southern (KCS) to the same review process and standards that govern CN's proposed voting trust. As explained below, CN's position is both contrary to law and fundamentally at odds with the very different factual contexts of the two voting trust proposals. Accordingly, we respectfully submit that the Board should proceed to review each of the pending voting trust proposals under the different regulatory review processes and standards applicable to each of them.

In short, it follows inexorably from the Board's decision to apply the KCS waiver to the CP/KCS transaction that CP's proposed use of a voting trust is subject to the pre-2001 merger rules, which are different from the Board's current regulations. See Finance Docket No 36500, Decision Nos. 3 (at 2 n.2) and 4 (at 3). It is already manifest that CP's proposal meets the pre-2001 standard, as it will effectively insulate KCS from premature control by CP. CN wholeheartedly agrees. See CN-6 at 4-7 (CN's supposedly "identical" voting trust agreement and trustee selection satisfies "longstanding and specific guidelines in part 1013"). Under well-established Board precedent (relied upon by CN), CP's proposed voting trust need only "ensure that it [is] not used to obtain unauthorized control of a regulated carrier," and CP's "submission of [the] voting trust for an informal opinion [is] purely voluntary." Union Pacific Corp., et al. - Request for Informal Opinion - Voting Trust Agreement, Finance Docket 32619, 1994 WL 680238, at *1 n.1, * 3 (ICC served 20 Dec 1994) (UP/Santa Fe).

CN's proposal, by its own admission, is subject to the 2001 rules, and their requirement that the Board conduct the "public interest" review mandated by new Section 1180.4(b)(4), which goes beyond consideration of whether the trust will insulate KCS from premature control.[2] The Board should proceed to establish a process for consideration of CN's proposal, in which CP intends to participate.

Though CP will in due course demonstrate why approval of CN's proposal to acquire the shares of KCS prior to obtaining control authorization is not in the public interest, CP wishes to expand briefly on why there is no merit to CN's suggestion that its trust proposal should be subject to the same review process as CP's proposal.

Different Factual Contexts Demand Different Treatment

CP begins by observing that CN's assertion that its voting trust proposal is "identical" to that proposed by CP is fundamentally incorrect. Although the terms of the proposed trust agreement itself, and the proposed trustee, appear to be substantially the same, that is where any similarity ends. The Board's 2001 rules require that any voting trust proposal be considered in the context of the specific transaction for which a trust would be used. 49 CFR § 1180.4(b)(4)(iv). Here, CN is proposing to use a trust to allow it to consummate its own acquisition of KCS prior to obtaining Board approval of CN's control of KCS, which raises fundamentally greater public interest concerns than CP's proposal.[3] Specifically:

1. Perhaps most fundamentally, CN and KCS are head-to-head horizontal competitors today, and that competition - notwithstanding the lack of CN premature control over KCS - would be adversely affected, perhaps permanently, by the change in incentives associated with CN's ownership of all of KCS's stock during the pendency of a lengthy control proceeding. The Department of Justice was correct to see these incentive effects as a concern where railroads compete, and in the case of a CN/KCS transaction those concerns actually apply. Finance Docket No. 36500, DOJ Comment (filed 12 Apr 2021) at 3-4.

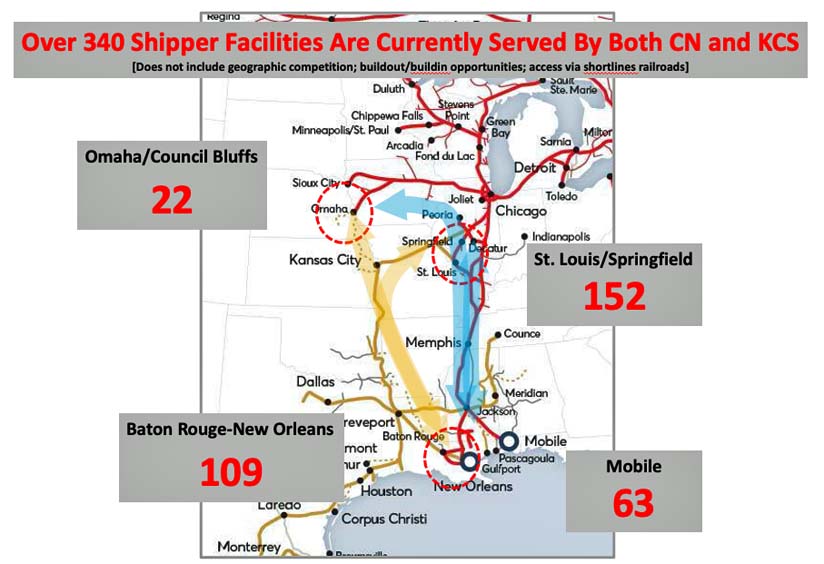

CN tries to sidestep this basic fact by asserting that DOJ's concerns do not apply to it because its transaction is "end-to-end." Finance Docket No. 36514, CN-6, at 12. That characterization is a blatant misrepresentation of the facts. Whereas CP's proposed transaction is in fact "end-to-end in nature" (see CP/KCS, Decision No. 4 at 2), a CN combination with KCS is not, as even a cursory glance at a rail map demonstrates. Both the substantially parallel nature of the CN and KCS systems and readily-available data on carrier access (direct and via reciprocal switch) confirm the substantially head-to-head overlap between the systems, as shown in Figure 1 below. In sum, more than 340 shipper facilities have service from both CN and KCS at locations across KCS's U.S. system (not including shippers benefitting from build-in/build-out competition, geographic competition, and access to both railroads via connecting shortlines).

Not surprisingly, then, when IC (CN's predecessor) sought to acquire KCS in 1994, major shippers in the Baton Rouge-New Orleans corridor objected to

the proposed use of a voting trust in that case because the proposed merger would have substantial adverse competitive impact. As they explained:

"Petitioners operate major petroleum and petrochemical production facilities in the Baton Rouge-New Orleans corridor and are served by one or both of the rail carriers involved in this merger proceeding. The ICR and KCSR run parallel routes between New Orleans and Baton Rouge, and are the only two carriers serving the chemical corridor along the east bank of the Mississippi River. While the routes thereafter diverge, they run essentially in parallel into the Midwest. Analysis of 1992 waybill data reveals approximately US$700 million of traffic originated or terminated in the Baton Rouge-New Orleans corridor, and the chemicals group constituted approximately 44 percent of that traffic. Petitioners alone account for approximately 5 Billion pounds of freight annually moving by rail in the corridor. A merger of the ICR and KCSR would have substantial adverse impact upon Petitioners by virtue of elimination of competition, heretofore imminent competition, and potential competition in the Baton Rouge-New Orleans corridor."

Illinois Central Corp. - Common Control - Illinois Central R.R. & The Kansas City Southern Ry., Finance Docket No. 32556, Petition of Bordon, Fina and Shell (filed 27 Sep 1994), at 2 (emphasis added). That transaction was abandoned after the ICC sought comment on the proposed trust arrangement.

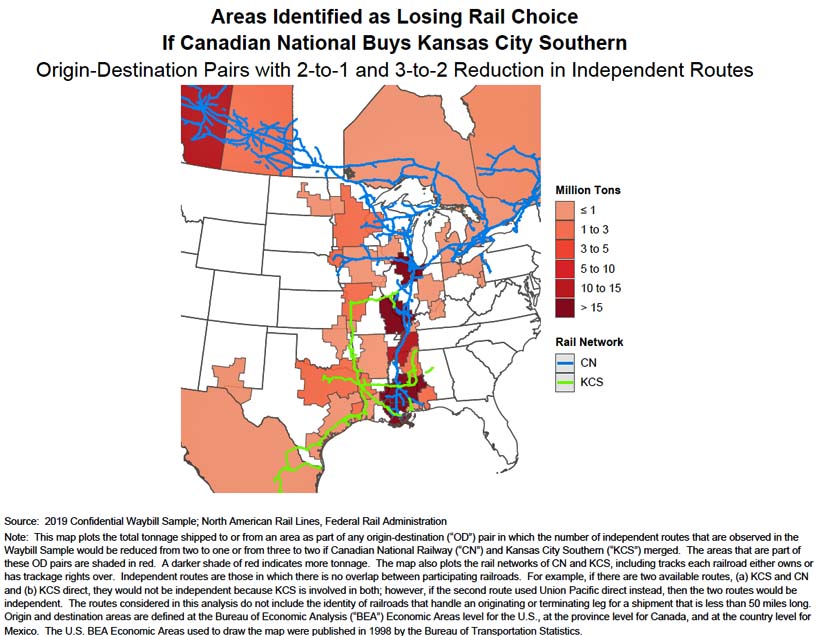

Confirming the very significant competitive issues raised by CN/KCS's horizontal merger, preliminary analysis of the Board's Waybill Sample data[4] shows that very substantial flows of traffic would suffer 2-to-1 or 3-to-2 reductions in independent rail routes as a result of a CN/KCS transaction, as shown in Figure 2 below:[5]

CN's proposed use of a trust would have immediate adverse effects on all of this competition and for well more than a year, regardless of what steps CN

might ultimately propose to remedy competitive concerns at the end of the regulatory review process.

2. Second, as explained in CP's 21 Apr 2021 Letter in Finance Docket 36500 (CP-12), unlike CP/KCS, a CN acquisition would uniquely destabilize the balanced structure of the North American railroad industry. By blocking CP's proposed acquisition of KCS, a closing of CN's acquisition into trust would leave CP asymmetrically disadvantaged and stranded north of Kansas City, creating strong strategic pressure for further consolidation. This would happen as soon as CN acquired KCS's stock and placed it in trust.[6]

3. Third, the ultimate outcome of the Board's regulatory review of a CN/KCS transaction (the first ever under the 2001 merger rules) is highly uncertain - certainly far more so than the CP/KCS transaction. The harms to competition a CN/KCS transaction and its impact on downstream consolidation - both of which are vital public interest factors under the 2001 rules - will have an important bearing on whether the Board could ever find that the CN/KCS transaction is consistent with the public interest as well as on the extensive conditions that would be required to make it so. Given this uncertainty, CN's proposal to place KCS into trust bears vastly more risk of a bad outcome for KCS, the industry, and perhaps even CN - no matter how well CN thinks its crystal ball is able to predict the Continent's late-2022 economic future and the implications of a forced divestiture process.

Different Regulatory Standards and Processes Must Govern

CN well understands that it would have no chance of prevailing were it to seek to have the KCS waiver applied to its proposed transaction, for all of the reasons summarized above. Instead, it effectively urges the Board to reconsider its Decision No. 4 (in Finance Docket No. 36500), which found that the KCS waiver does apply "neatly" to CP's proposed acquisition of KCS.

1. The inherent consequence of that decision is that the pre-2001 Board regulations and precedent apply to CP's voting trust proposal. The Board has already noted that its waiver decision determines which "regulations pertaining to voting trusts" shall apply. Finance Docket No 36500, Decision Nos. 3 at 2 n.2. The new "public interest" review of voting trusts was added by the 2001 rules, and did not exist previously. This precise point was made by the Board when it revised its merger rules in 2001: "The Board, like the ICC before it, has permitted the use of voting trusts during the pendency of control applications, so long as the trust would not result in unlawful control. 49 CFR 1013."

The Board's pre-2001 precedent governing the use of voting trusts is thus well-established and unambiguous: voting trusts are permitted when they effectively insulate the target from premature control, pure and simple. The Board's regulations (49 CFR § 1013) and countless pre-2001 major merger (and post-2001 other merger) precedents speak to this. E.g., UP/Santa Fe, at * 3 (scrutinizing "proposed voting trust and, as revised here, find[ing] nothing inherent in its provisions that would result in the kind of premature, unauthorized, control prohibited by the ICA"); Canadian National Ry., Grand Trunk Corp., & Grand Trunk Western R.R. - Control - Illinois Central Corp., Illinois Central R.R., Chicago, Central & Pacific R.R., & Cedar River R.R., Letter from Vernon A. Williams to Paul A. Cunningham (25 Feb 1998) (providing informal opinion that proposed trust would effectively insulate acquirer from a control violation). Accordingly, the path for further review of CP's proposed trust is clear based on the Board's decision that the pre-2001 rules would apply to the CP/KCS transaction. There is no occasion for any further review process given that it is acknowledged that under Board precedent CP's proposal will insulate KCS from premature control.

CN's suggestion that the Board should conduct a further or different review of CP's proposed use of a trust is contrary to Board precedent and inappropriate in light of the very different factual circumstances posed by the two pending proposals. CN would at minimum be required to satisfy the stringent standards for seeking reconsideration of the Board's ruling in Decision No. 4, but it does not even attempt to do so.

2. The regulatory path for CN's proposed trust is equally clear, but very different. CN has now moved for approval of its trust under the Board's 2001 rules. It has not sought a waiver of the 2001 rules, in whole or in part but has affirmatively embraced them. E.g., CN 26 Apr 2021 Letter at 2 ("CN remains committed to the current merger rules"). Therefore, it expressly invokes the public comment process set forth in new Section 1180(b)(iv) for review of its trust proposal. Finance Docket 36514, CN-6 at 17. The Board should proceed to establish a public comment period.

3. If CN's 26 Apr 2021 letter is instead intending to suggest that CN's voting trust proposal should be governing by the same pre-2001 standards as apply to CP's proposal, that request is procedurally improper and substantively misguided. At minimum, to attain the procedural posture it seeks, CN would first have to propose a waiver of the 2001 rules, which it has both opposed and renounced for purpose of its own transaction. If CN nonetheless intends to seek a waiver, the Board's regulations provide for objections by interested parties within ten days. 49 C.F.R. § 1180.0. (b). CP certainly would object for the reasons set forth above, but other interested parties must also have the opportunity to know that a waiver is being sought and submit their own comments on its appropriateness.

4. Finally, CN's suggestion that the Board review the two trust proposals simultaneously is meritless, not just because different standards and processes apply to them. It would be manifestly unjust to hold up CP's voting trust proposal awaiting a process for review of CN's proposal that CN has chosen to wait to commence for a full month after CP announced its agreement with KCS and CP and KCS jointly filed their Notice of Intent.

* * *

For the foregoing reasons, CP requests that the Board proceed with each of the pending voting trust proposals under the different regulatory review processes and standards that apply to them. CP appreciates the Board's attention to this matter.

Respectfully submitted,

David L. Meyer - Attorney for Canadian Pacific Railway Limited

cc: All Parties of Record in Finance Docket Nos. 36500 and 36514

[1] Canadian Pacific Applicants are Canadian Pacific Railway Limited, Canadian Pacific Railway Company, and their U.S. rail carrier subsidiaries Soo Line Railroad Company, Central Maine & Quebec Railway US Inc., Dakota, Minnesota & Eastern Railroad Corporation, and Delaware & Hudson Railway Company, Inc. (collectively "Canadian Pacific" or "CP").

[2] See 49 CFR § 1180.4(b)(4)(iv) ("applicants contemplating the use of a voting trust must explain how the trust would insulate them from an unlawful control violation and why their proposed use of the trust, in the context of their impending control application, would be consistent with the public interest") (emphasis added).

[3] Although a question better addressed in the context of the public interest review of CN's proposed trust, CN's suggestion that the impact on CN's finances is the only relevant public interest factor is wrong. That assertion is flatly inconsistent with both the breadth of the Board's "public interest" discretion (e.g., Penn-Central Merger and N&W Inclusion Cases, 389 U.S. 486, 498-99 (1968) ("determination of the factors relevant to the public interest is entrusted by the law primarily to the Commission, subject to the standards of the governing statute") and the Board's conclusion in 2001 that use of voting trusts "should be available only for those rare occasions when their use would be beneficial." Major Rail Consolidation Procedures, Ex Parte No. 582 (Sub-No. 1) (STB served 11 Jun 2001) at 29-30 n.29.

[4] CP's use of these data was for purposes of Finance Docket No. 36500, in order to respond to CN's claim in that docket that the implications of the two voting trust proposals are identical.

[5] CN seems to believe that it need not address - via remedy or otherwise - competitive harm except where CN and KCS are the only serving rail carriers. Finance Docket No. 36500, CN 23 Apr 2021 Letter at 3 ("If KCS chooses to partner with CN, CN will propose effective solutions, working closely with these customers to ensure that no customer will become sole served as a result of the transaction."). This is a misguided viewpoint. Even if one adopted an "only 2-to-1 harm matters" perspective, given the broadly parallel nature of the CN and KCS systems south of Kansas City and Springfield, Illinois, much of the traffic suffering adverse competitive impacts in fact involves 2-to-1 reductions in viable routing alternatives despite specific shipper facilities being served by more than two carriers (such as where the two best routes between origin and destination involve CN and KCS, which CN proposes to reduce to a single carrier, CN).

[6] Indeed, CP is very concerned that CN would downgrade KCS's mainline north of Shreveport, undermining potential future CP/KCS interline options

regardless of any commitment CN might make to keep the Kansas City gateway "open."

(because there was no image with original article)

(usually because it's been seen before)

provisions in Section 29 of the Canadian

Copyright Modernization Act.